Discover the best cryptocurrency tax tips in the USA. Learn IRS rules, reporting strategies, and ways to reduce your crypto tax burden legally.Cryptocurrency trading and investing have exploded in popularity across the United States. Whether you’re buying Bitcoin, staking Ethereum, or trading altcoins, one fact remains unavoidable: the IRS wants its share of your profits.

Unfortunately, crypto taxes can feel confusing. From reporting gains to understanding staking rewards, the rules often leave investors scratching their heads. This guide breaks down the top cryptocurrency tax tips in the USA so you can stay compliant, avoid penalties, and even reduce your tax liability legally.

1. How the IRS Treats Cryptocurrency

The IRS does not consider crypto as “currency.” Instead, it’s classified as property. This means:

- Capital Gains Tax applies when you sell, trade, or use crypto.

- Ordinary Income Tax applies to rewards from mining, staking, or earning crypto.

👉 Example:

- If you bought 1 Bitcoin at $20,000 and sold it at $30,000, you owe tax on the $10,000 gain.

- If you earned 0.5 ETH from staking, it’s taxed as income at fair market value on the day you received it.

2. Key Cryptocurrency Taxable Events in the USA

Not all crypto activities are taxable. Here’s what triggers taxes:

✅ Taxable Events

- Selling crypto for USD

- Trading one cryptocurrency for another

- Using crypto to buy goods or services

- Receiving staking, mining, or airdrop rewards

- Getting paid in crypto for freelance or work

❌ Non-Taxable Events

- Buying and holding crypto (no sale)

- Transferring crypto between your own wallets

- Donating crypto to a registered charity (can be tax-deductible)

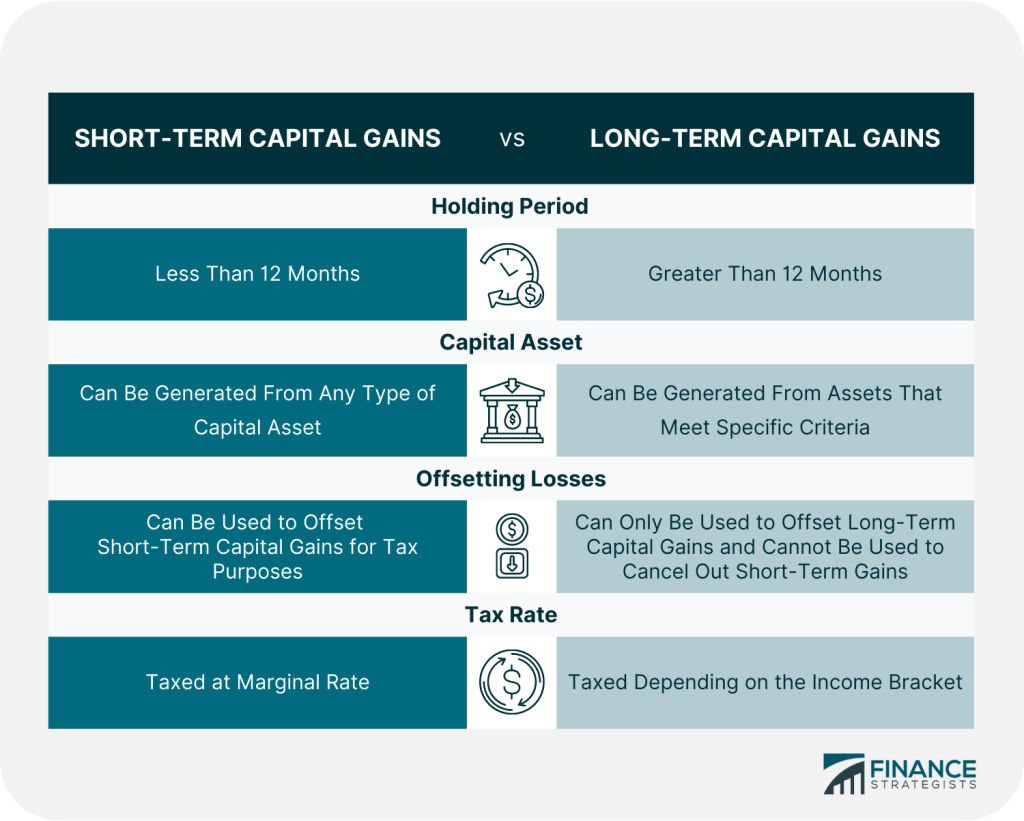

3. Short-Term vs Long-Term Capital Gains

Your tax rate depends on how long you hold your cryptocurrency:

- Short-Term Capital Gains: Held less than 12 months, taxed at your ordinary income tax rate (10%–37%).

- Long-Term Capital Gains: Held more than 12 months, taxed at 0%, 15%, or 20% depending on income.

👉 Tip: Holding crypto for over a year can significantly reduce your tax bill.

4. Top Cryptocurrency Tax Tips in the USA

1. Keep Detailed Records

- Track every trade, transfer, and wallet activity.

- Use crypto tax software like CoinTracker, Koinly, or TokenTax.

- The IRS requires date, amount, fair market value, and purpose for each transaction.

2. Use Tax-Loss Harvesting

- Offset gains with losses.

- Example: If you made $8,000 profit on Bitcoin but lost $5,000 on altcoins, you only pay tax on $3,000.

- Up to $3,000 in losses can also be deducted against ordinary income.

3. Consider Long-Term Holding

- If possible, hold crypto for 12+ months before selling to qualify for lower capital gains tax rates.

4. Report Crypto Income Correctly

- Mining and staking rewards = ordinary income.

- Airdrops = taxable as income at fair value.

- Freelancing or payments in crypto = income tax applies.

5. Donate Crypto for Tax Benefits

- Donating to IRS-approved charities can reduce your taxable income.

- Bonus: No capital gains tax on appreciated crypto donations.

6. Use Retirement Accounts for Tax Advantages

- Self-Directed IRAs (SDIRAs) allow you to hold Bitcoin and other crypto with tax-deferred or tax-free growth.

7. File Form 8949 and Schedule D

- Report capital gains and losses on Form 8949.

- Attach it to your Schedule D and include it in your federal tax return.

5. Common Mistakes to Avoid

- ❌ Thinking the IRS won’t know: Exchanges like Coinbase and Kraken report transactions.

- ❌ Forgetting small trades: Even swapping ETH for USDT is taxable.

- ❌ Not reporting staking or mining rewards.

- ❌ Ignoring state-level crypto taxes (varies by state).

- ❌ Waiting until the last minute (penalties for late filing can be steep).

6. Best Crypto Tax Software for USA Users

- CoinTracker – integrates with Coinbase, Binance, Kraken.

- Koinly – supports 700+ exchanges, DeFi, and NFTs.

- TokenTax – best for complex portfolios with multiple wallets.

👉 Related Read: Best Crypto Exchange for Beginners

7. Future of Crypto Taxes in the USA

The IRS is tightening enforcement:

- Exchanges must issue 1099 forms by 2025.

- Crypto tax reporting will become as standard as stock reporting.

- DeFi and NFT transactions will soon have clearer tax guidance.

FAQs on Cryptocurrency Taxes USA

1. Do I need to report crypto if I only lost money?

Yes. Even if you lost money, you must report transactions. The good news is losses can offset gains.

2. Is transferring crypto between wallets taxable?

No. Moving crypto from Coinbase to your hardware wallet is not taxable.

3. Can the IRS track my crypto transactions?

Yes. Most exchanges issue 1099 forms and share data with the IRS. Blockchain transactions are also traceable.

Conclusion

Cryptocurrency taxes in the USA may feel overwhelming, but with the right strategy, you can stay compliant and even save money legally. Keep records, use tax-loss harvesting, report income correctly, and consider long-term holding for better tax rates.

Final Tip: Consult a certified tax professional specializing in cryptocurrency to ensure you’re filing correctly and optimizing your returns.